Vendor Insurance for CRE Teams Managing Third-Party Contractors

Key takeaways:

- Vendor insurance refers to policies third-party service providers carry to protect themselves and clients from liability when vendor work causes injuries or property damage.

- Property teams require vendor insurance to transfer financial liability to the vendor's insurer, preventing exposure from incidents that could otherwise result in multi-million dollar settlements, premium increases, and coverage restrictions.

- Visitt automates vendor insurance compliance, validating coverage and tracking renewals within the property management platform to ensure continuous vendor compliance across portfolios.

What is vendor insurance?

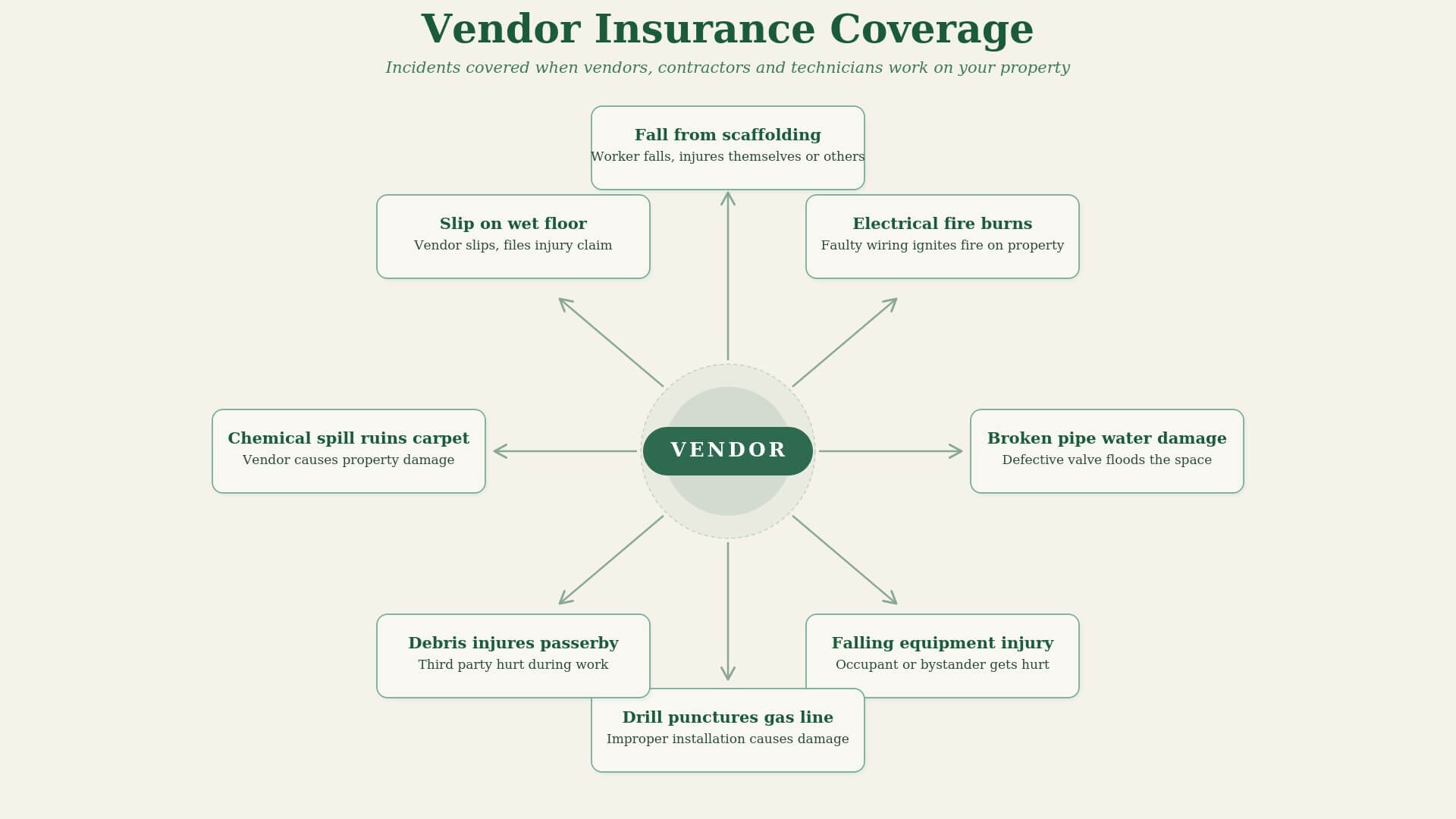

Vendor insurance refers to the specific insurance policies that third-party service providers must carry to protect themselves and their clients from liability linked to work-related incidents:

- Third-party bodily injury: Medical expenses and legal defense when someone gets hurt because of the vendor's operations

- Property damage to others: Repair or replacement costs when the vendor damages client property commercial property maintenance

- Product-related claims: Coverage for injuries or damage caused by products the vendor installs or supplies

- Legal defense and settlements: Attorney fees, court costs, and judgment payments for covered claims that could otherwise drain operating capital

When incidents occur, vendor liability insurance pays out a portion of the provider's liability, covering legal fees and settlement payouts for valid claims against the vendor. The vendor certificate of insurance documents these protections, allowing clients to verify coverage before work begins and understand what is guaranteed in terms of financial responsibility.

Note: This specific coverage does not protect the vendor's own equipment or inventory.

Types of vendor insurance

Different vendors need different types of liability coverage, based on the services they provide and the specific risks those services create:

- General liability insurance: The foundational policy most clients require from every vendor. Covers bodily injury and property damage claims related to vendor operations.

- Professional liability insurance: Also called errors and omissions (E&O) coverage, this protects vendors who provide consulting, design, or advisory services. When an energy consultant recommends equipment maintenance strategies that fail to deliver promised energy efficiency in commercial buildings, or when a safety engineer's specifications prove inadequate during commercial property inspections, professional liability coverage handles the resulting claims.

- Workers' compensation insurance: Required by law in most jurisdictions, it covers medical or rehabilitation treatment and lost wages when vendor employees are injured on the job.

- Commercial auto insurance: Mandatory for vendors who use vehicles for transportation, deliveries, or mobile services. Covers property damage and bodily injury from accidents occurring while vendors travel to and from job sites.

- Umbrella insurance: Secondary coverage that activates after primary policies reach their limits, often required for high-value or particularly hazardous work.

- Product liability insurance: Covers claims related to defective products that vendors manufacture, distribute, or install.

What are specific vendor insurance requirements for commercial real estate (CRE)?

Property teams must ensure their vendors meet specific insurance requirements that address the unique risks of commercial real estate property management. These vendor insurance requirements span different coverage types and compliance standards based on the nature of work being performed, whether preventive maintenance, predictive maintenance, office maintenance, or other building operations that create concentrated liability exposure in occupied facilities.

Why do commercial real estate teams need vendor insurance management?

Vendor insurance functions as a risk management strategy, determining who absorbs financial liability following incidents at commercial properties. The following case is commonly cited by property management firms and law offices as a cautionary tale:

A maintenance contractor performing facade repairs on a New York property triggered an incident where the vendor's employee fell through an unprotected opening in the first floor and fractured a thoracic vertebra, rendering him paraplegic. The employee received workers' compensation but also sued the property owner under New York Labor Law Section 240, which imposes absolute liability on property owners for gravity-related injuries regardless of who employs the injured worker. Because the property owner had verified the vendor certificate of insurance and required additional insured endorsements, the vendor's employer's insurer paid $7 million plus waived a $150,000 workers' compensation lien to settle the suit. Without proper vendor insurance coverage, the property owner would have faced the entire $8.2 million liability!!!

Operational and financial risks from inadequate vendor insurance oversight:

- Uninsured repair costs, when vendor liability insurance excludes specific damage types like workmanship defects

- Lost rental income, during repairs, until occupancy is restored

- Legal defense expenses from vendor incidents, with costs accumulating regardless of case merit

- Premium increases after major claims, with elevated premiums persisting for multiple renewal cycles

- Coverage restrictions–exclusions or limitations–on future claims, following vendor-related incidents

- Property devaluation, as buyers and lenders price in liability concerns from recurring vendor issues

- Regulatory penalties from vendor work that doesn't meet code standards trigger fines separate from insurance claims

Solutions for managing vendor insurance requirements:

- Deploy automated certificate of insurance tracking: Use facility management software to verify vendor insurance coverage limits against contract requirements and receive alerts before coverage lapses across asset lifecycle management.

- Verify insurance before starting: Require vendor COI documentation 7-14 days before authorizing any vendor work.

- Lean on insurance specialists: Hire experts or use digital platforms to review policy language for exclusions, endorsements, and state-specific requirements, ensuring adequate protection.

- Educate vendors on compliance: Communicate insurance requirements for vendors during onboarding through document management systems and explain financial consequences of non-compliance, including contract termination and liability exposure.

- Monitor coverage across portfolios: Implement maintenance management software and use operations dashboards to consolidate vendor insurance data across properties, identifying which vendors create liability gaps requiring immediate attention through risk management protocols.

What goals does vendor liability insurance help CRE firms achieve?

Vendor liability insurance serves multiple strategic purposes across the vendor-CRE firm relationship, which your insurance software vendor can help you achieve:

- Transfers financial responsibility for accidents and damages to the vendor's insurer, protecting the property owner's balance sheet and insurance loss history when incidents occur during work.

- Prevents vendor bankruptcies from large liability claims, ensuring that critical services continue without disruption, even when legal disputes arise.

- Meets regulatory and lender requirements that mandate minimum coverage levels for third-party contractors working in commercial properties, avoiding penalties and compliance violations.

- Protects tenant experience during vendor incidents by funding immediate repairs and injury claims when vendor work damages amenities or injures occupants, preventing disputes and service delays that would otherwise trigger complaints through tenant communication tools.

- Reduces insurance premiums for property portfolios by demonstrating strong risk management to property insurers and supporting lower premium negotiations during policy renewals

How does Visitt help CRE teams manage vendor insurance requirements?

Visitt embeds vendor insurance compliance directly into its commercial real estate property management platform, running inside the same centralized system teams use for work order management and other building operations. The platform’s AI-powered COI Agent reads contract requirements, requests certificates, validates coverage against property-specific limits, and tracks renewals automatically. Risk-based insurance requirements can be defined by trade type or risk tier, allowing different coverage levels to be applied automatically for HVAC maintenance, commercial property maintenance, or preventive maintenance contractors. And the platform only routes cases it cannot resolve to operations teams while handling routine compliance tasks without manual intervention.

Thanks to Visitt, property teams can consistently ensure vendor compliance data and risk management decisions stay aligned across commercial property portfolios.

See how Visitt streamlines vendor insurance tracking across your portfolio.